Recent News

Current Thoughts and Comments |

February 10, 2025

January Market Review

Dear Clients and Friends:

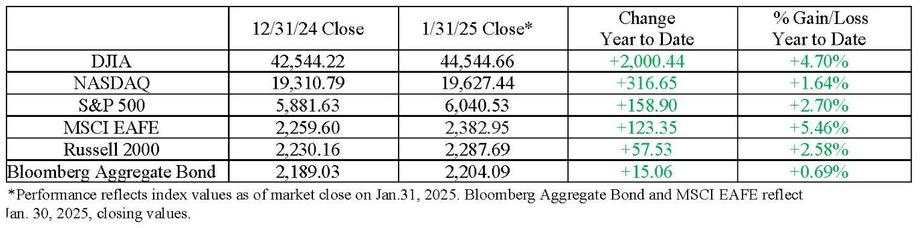

Despite uncertainty surrounding inflation, interest rates, the political landscape and a new disruptor in the artificial intelligence (AI) race, domestic equities ended the first month of 2025 broadly positive, reflecting a continuing optimism for the U.S. economy.

AI-themed stocks, which have pulled headline indices upward for the past two years, were shaken by a new entrant into the space, China’s DeepSeek, which claims to be more efficient in various ways, especially power consumption, than key competitor OpenAI’s ChatGPT. DeepSeek’s unveiling also took a toll on energy and utility sector stocks, which were benefiting from an expectation that growth in power-hungry AI would spike electricity demand.

“With mega-cap tech valuations stretched, those companies were vulnerable to a pullback,” said Raymond James Chief Investment Officer Larry Adam. “While the NASDAQ took most of the hit, the performance of the equal-weight S&P 500 versus the capitalization weighted index shows signs of the market broadening beyond tech that we hope will continue.”

Amid the many changes that greeted the new year, including the inauguration of President Donald Trump, the Federal Reserve held interest rates constant, as expected, as the Federal Open Market Committee (FOMC) awaits clear signs that inflation will continue to slide toward target levels and insight into the federal government’s trade and fiscal priorities.

Before we dive into the details, let’s see how we started 2025:

Employment strong as price pressures continue

December saw higher-than-expected employment growth, but overall contraction. The rate of unemployment decreased modestly as total employment increased strongly. Although we expect the total job creation number for 2024 to be shaved down once the benchmarks come in later this year, growth was still significant.

Short-term volatility may dampen overabundant enthusiasm

Consistent with the amount of uncertainty in the market regarding inflation, interest rates, fiscal and trade policy, and the potential disruption to domestic AI dominance from China, market volatility increased throughout December and January. A period of anxiety can be beneficial, however, a market free of pessimism can unbalance risk and reward expectations, pushing investors toward untenable positions.

Treasury yields end up flat despite turbulence

Producer Price Index and Consumer Price Index data, used to gauge inflation, came out mostly on target, pushing Treasury yields back down. They ended the month with minimal net change despite having bounced around significantly in January. The one-month Treasury Bill increased five basis points, the largest rate move of any point on the Treasury curve last month. The January 28-29 FOMC meeting decided to leave the fed funds rate unchanged as expected.

The new administration previews key themes

The initial days of the second Trump administration revealed several important things to watch for. The flurry of executive orders included actions ranging from symbolic gestures to unilateral policy decisions. Time will tell how many make it past legal challenges and Congressional authorization. The executive order on trade policy lays out a roadmap including tariffs – ranging from universal to sector-specific – and ramps up restrictions on the flow of tech to China.

Energy policy changes may be sidelined by producers’ strategies

The oil and gas industry rarely exceeds its predetermined budget when it comes to investing in new drilling and infrastructure, which could dampen the effect of the new U.S. administration’s pro-production priorities. Despite goals to lower energy prices by increasing domestic oil and gas production, the slowing demand for oil on a global scale over the past two decades is reflected in the restriction of preplanned expenditure among producers in an effort to return more capital to shareholders.

Global markets uncertain as the US pivots toward domestic priorities

A period of ambiguity for international economies now looms as the U.S. shifts its economic priorities inward. The UK had a rough start to the year with sovereign bond yields plummeting to their lowest since 1998 as the economy flatlined. A weak fiscal position drove sterling down against the dollar on the foreign exchange. China faced continued headwinds and Japan raised interest rates by 25 basis points to 0.50% as efforts to move sustainably toward its 2% inflation target bear fruit.

The bottom line

The year started off strong, but time will tell whether that trend will hold. Uncertainty remains a familiar theme moving forward as inflation remains sticky and the policy decisions of a new administration begin to take shape. Expect volatility and emotional reactions in the markets in the coming months, but with a positive overall trend throughout the year.

We remain committed to the pursuit of your financial goals and thank you for your continued trust in our guidance. If you have any questions about this report, or need help with anything at all, please don’t hesitate to contact us.

Broadening Our Horizons - Practice the positive mindset of Susan B. Anthony

February 15 marks the birthday of Susan B. Anthony, the social reformer, journalist, publisher and women’s rights activist. Throughout her life, she understood the importance of focusing on the shape of things to come and not allowing past mistakes to undermine the future.

A reporter once asked her how she’d endured decades of working for women’s voting rights with more losses than wins to show for her efforts. She responded, “Defeats? There have been none. We are always progressing.”

Her activism began with the Daughters of Temperance, fighting against the prevalence and ill effects of alcoholism. Barred from speaking at rallies where men attended, Anthony found another way to make her voice heard: she spearheaded the women’s suffrage movement.

In 1866, she and pioneering suffragette Elizabeth Cady Stanton formed the American Equal Rights Association. This association, along with decades of tireless work from Anthony and Stanton, would go on to radically change the American social landscape for the better. Although Anthony passed away 14 years before women won the right to vote, her relentless work and refusal to give up paved the way for greater rights for the generations of women to come.

Everyone faces trials and tribulations in life, but what is crucial – what Anthony exemplified most – is how important it can be to continue moving forward. Perhaps she said it best over a century ago: “Forget conventionalisms; forget what the world thinks of you stepping out of place; think your best thoughts, speak your best words, work your best works, looking to your own conscience for approval.” Good words to live by as you strive toward your own goals, don’t you think?

Please note that our office, along with the financial markets, will be closed on Monday, February 17th, in honor of Presidents Day. Remember, you can always access your account(s) online using Client Access.

We also hope you have a wonderful Valentine’s Day. No matter how you choose to share the love on this special day, we hope your holiday is filled with the people and things that mean the most to you!

Sincerely,

Tricia L. Tripp, CPA, CFP®

Financial Advisor

Securities offered through Raymond James Financial Services, Inc. Member FINRA/SIPC. Investment Advisory Services are offered through Raymond James Financial Services, Inc. Tripp Financial Consultants, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services, Inc.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Raymond James Chief Investment Officer and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. Diversification does not guarantee a profit nor protect against loss. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australasia and Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small-cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges, which would reduce an investor’s returns. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification. A credit rating of a security is not a recommendation to buy, sell or hold the security and may be subject to review, revision, suspension, reduction or withdrawal at any time by the assigning Rating Agency. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Income from municipal bonds is not subject to federal income taxation; however, it may be subject to state and local taxes and, for certain investors, to the alternative minimum tax. Income from taxable municipal bonds is subject to federal income taxation, and it may be subject to state and local taxes. Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. The Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Studies. The Leading Economic Index (LEI) provides an early indication of significant turning points in the business cycle and where the economy is heading in the near term. This is not a recommendation to purchase or sell the stocks of the companies pictured/mentioned. Investing in small-cap stocks generally involves greater risks, and therefore, may not be appropriate for every investor. The prices of small company stocks may be subject to more volatility than those of large company stocks. The Nikkei 225 is a stock market index is for the Tokyo Stock Exchange (TSE). It is the most widely quoted average of Japanese equities. The ISM Services Index is an economic index based on surveys of more than 400 non-manufacturing (or services) firms' purchasing and supply executives. The ISM Manufacturing Index, also known as the purchasing managers' index (PMI), is a monthly indicator of U.S. economic activity based on a survey of purchasing managers at more than 300 manufacturing firms.

Material created by Raymond James for use by its advisors.